Updated April 2026

People can only make wise money management decisions by understanding basic financial concepts, spending less on transaction fees, accumulating less debt, and paying lower interest rates on loans. Being financially literate allows you to make sound decisions about saving, investing, borrowing, and budgeting more effectively.

This post reveals financial literacy statistics and facts you need to know in 2026. We examine global variations in financial literacy by country, gender, and generation, with particular attention to financial knowledge and capability among kids and young adults. How many Americans are financially literate? What about the UK? Let’s grasp essential statistics on financial literacy.

Financial Literacy Statistics Highlights

-

- Only 33% of adults are financially literate globally, and U.S. adults answered only 49% of personal finance questions correctly in 2025.

-

- The United States ranks 14th in financial literacy globally.

-

- Gen Z has the lowest level of financial literacy in the US, correctly answering just 38% of index questions.

-

- 69% of Americans report that financial uncertainty has made them feel depressed and anxious (up from 61% in 2023).

-

- Only 23% of children frequently talk about money with their parents.

-

- British men are more financially literate than women.

-

- Only 23% of Brits passed the latest comprehensive financial literacy test — down sharply from 27% in 2023.

Global Financial Literacy Statistics and Facts

-

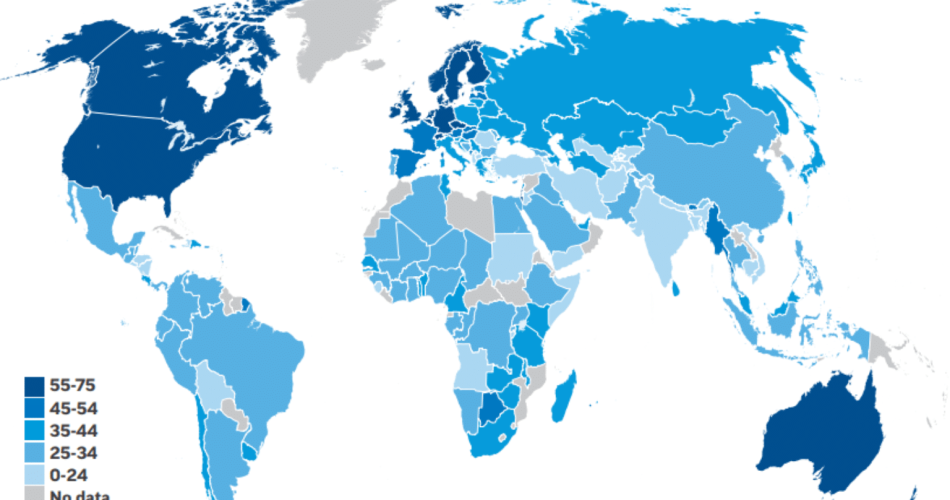

- Only 33% of adults are financially literate worldwide [1]. This figure, drawn from the most comprehensive global survey conducted by Standard & Poor’s, indicates that approximately 3.5 billion adults globally do not understand basic financial concepts, implying significant inequalities in financial knowledge. The threshold for being considered financially literate was understanding three out of four basic financial concepts: basic numeracy, risk diversification, compound interest, and inflation. This underscores the ongoing need for financial education initiatives worldwide.

-

- 65% or more of adults are financially literate in Australia, Canada, Denmark, Finland, Germany, Israel, the Netherlands, Norway, Sweden, and the United Kingdom [2]. These developed nations have the highest financial literacy rates worldwide, according to the S&P Global FinLit Survey. Northern Europe continues to show the strongest understanding of economic principles, while South Asia has the lowest rates, with only a quarter or fewer people financially knowledgeable.

-

- The United States ranks 14th in financial literacy globally [3]. While not the lowest, this ranking is concerning given that the US is the world’s largest economy. Sweden and Norway lead globally, with approximately 71% of their populations financially literate [3].

-

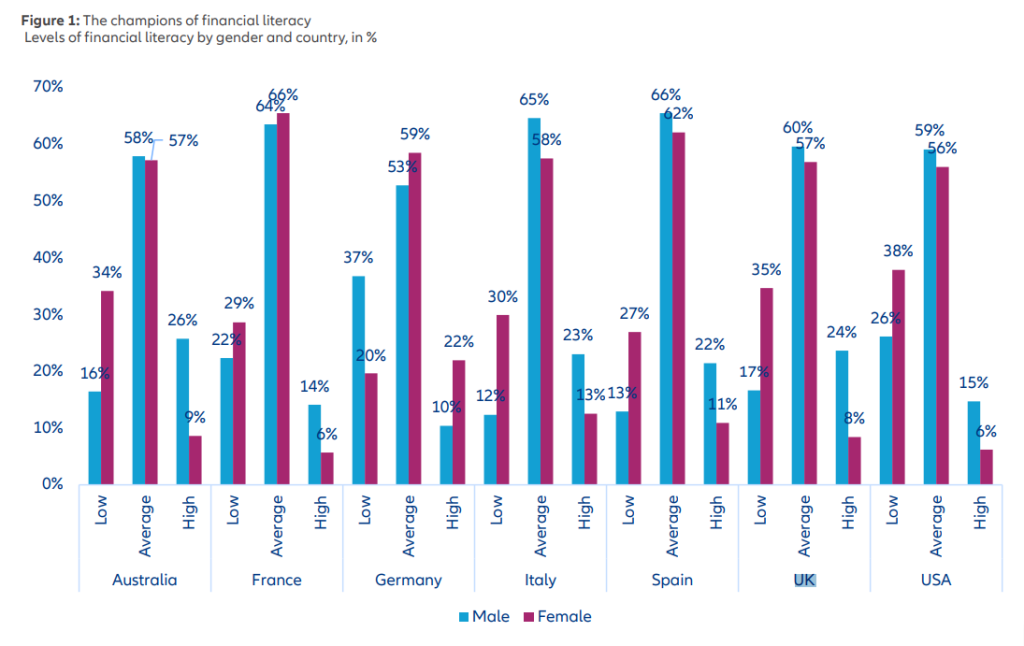

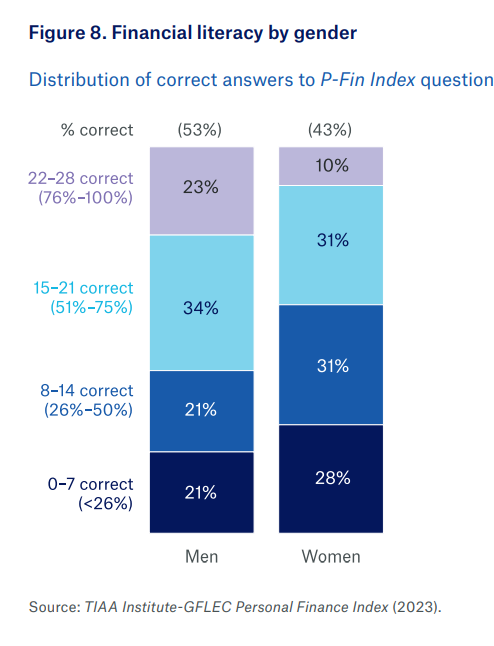

- There is a persistent gender gap, with women scoring lower on financial literacy globally [4]. Men are slightly more financially literate (35%) than women (30%) globally, according to the S&P survey. In the US, men correctly answer about 56% of P-Fin Index questions compared to around 46% for women — a gap that is roughly double the global average [5]. Germany is notable for being the one major country where women outperform men in the high financial literacy category [4].

-

- On a global scale, financial literacy increases with age [6]. Baby Boomers (born 1946–1964) have a higher concentration of high financial literacy than other groups, while Gen Z (born 1996–2003) scores the lowest. This is a consistent global pattern: the Silent Generation and Baby Boomers average around 55% on financial knowledge assessments, while Gen Z averages around 38% [6].

Financial Literacy Statistics in the United States

Facts and Statistics Among US Adults

-

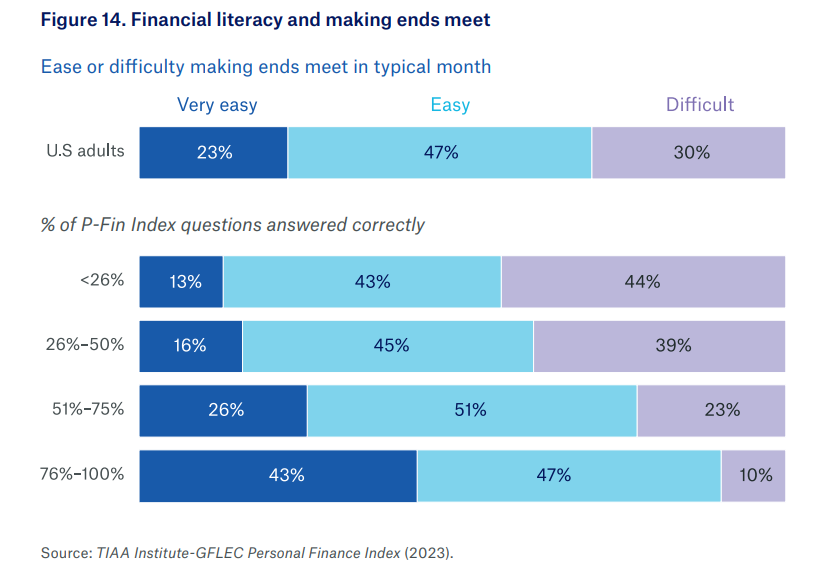

- U.S. adults correctly answered only 49% of P-Fin Index questions in 2025 [7], according to the 9th annual TIAA Institute–GFLEC Personal Finance Index — the same level as when the study began in 2017, and lower than the 52% recorded in 2020. This stagnation shows that no meaningful progress in basic financial knowledge has been made in nearly a decade. Fewer than half of adults (48%) answered more than half of the index questions correctly [7].

-

- 69% of Americans report that financial uncertainty has made them feel depressed and anxious [8], according to the 2025 Northwestern Mutual Planning & Progress Study — an 8-percentage-point increase over 2023. Multiple other surveys confirm the scale of financial stress: a separate 2025 survey found that 77% of Americans feel anxious about their financial situation [9], and a Betterment study recorded financial anxiety among full-time employees at an all-time high of 90%, with inflation (65%), credit card debt (40%), and housing costs (31%) as the top stressors [10].

-

- White and Asian Americans score the highest on financial literacy tests [5]. According to the 2025 P-Fin Index, White and Asian adults tend to answer over 50% of questions correctly. Black adults answer around 34% correctly on average, and Hispanic adults score slightly higher at 38%. These persistent gaps reflect long-standing disparities in access to financial education [5].

-

- Financial illiteracy costs Americans an estimated $246 billion collectively per year, or approximately $948 per person annually, according to the National Financial Educators Council’s 2025 survey [11]. Those with very low financial literacy levels are twice as likely to be debt-constrained and three times more likely to be financially fragile [7].

-

- Americans now owe $1.277 trillion in credit card debt [12], as of the fourth quarter of 2025, according to Federal Reserve data — a new record high and a significant jump from the $986 billion reported in early 2023. The average cardholder balance stands at approximately $6,523 [13]. About 47% of American credit cardholders carry a balance month to month [14]. Total US household debt reached $18.57 trillion as of September 2025, up 3.5% from the prior year [15].

-

- Gen Z has the lowest level of financial literacy in the US [7]. According to the 2025 TIAA Institute–GFLEC P-Fin Index, Gen Z correctly answered only 38% of index questions on average, far below Baby Boomers and the Silent Generation (55%), Gen X (49%), and Millennials (46%). Functional knowledge among Gen Z is substantially lower across every category compared with older generations [7].

-

- U.S. adults with greater financial literacy have better economic well-being [7]. Nine years of data from the TIAA Institute–GFLEC P-Fin Index confirm that adults with higher financial literacy are better prepared for retirement and more financially resilient. Those with very low literacy are three times more likely to be financially fragile [7].

-

- The financial literacy of American women frequently lags behind that of men [5]. The 2025 P-Fin Index shows a roughly 10-percentage-point gender gap in correct answers. Women are also more likely to select “I don’t know” when answering questions (25% vs. 20% for men), even when controlling for actual knowledge levels. This gap is present across all functional areas, including borrowing, saving, investing, insuring, and comprehending risk [5].

-

- Americans with a college degree are significantly more financially knowledgeable than those without one [16]. Research consistently shows that financial literacy rises with educational attainment, with adults holding tertiary education being approximately 20 percentage points more likely to be financially literate than those with only primary education [16].

Facts About US Kids’ and Youth’s Financial Knowledge

-

- 74% of US teens lack confidence and knowledge about personal finance [17]. Three in four American teenagers are not confident about their financial literacy. Many have never prepared a budget, and significant gaps persist around understanding credit, debit, and taxes.

-

- 73% of American teenagers want more financial education [18]. Most teens recognize the importance of financial literacy. They are particularly interested in content on YouTube (38%), TikTok (33%), and Instagram (25%). According to updated data, nearly 70% of Gen Z adults now turn to TikTok or YouTube to learn about money [19] — a trend that is growing rapidly, though the quality and accuracy of such advice varies widely.

-

- Only 23% of children frequently talk about money with their parents [20]. According to the Money Confident Kids Survey, less than a quarter of children have meaningful financial discussions at home, making school-based financial education critical.

-

- The gender gap in financial knowledge emerges at the age of 13 [17]. Only 21% of girls are confident about their personal finance knowledge, compared to 33% of boys. Girls are more likely to learn about contributing and giving, while boys are more likely to know about stock investing.

-

- 30 US states now require high schools to teach a standalone financial literacy course for graduation [21], up from 23 in 2023 and just 6 in 2019. Kentucky, Colorado, Texas, and Delaware all passed full graduation requirement bills in 2025 [21]. An additional 11 states allow financial literacy courses to substitute for other graduation requirements, meaning a total of 41 states have some form of personal finance education requirement [22]. Nineteen bills are still pending in seven more states [21].

To bridge the gap between financial theory and daily practice, parents are increasingly turning to specialized banking solutions designed for children and teens. On our website, we provide in-depth analysis to help you choose the right platform for teaching budgeting and saving skills. For a detailed breakdown of the top players, you can explore our comparisons of GoHenry vs. Greenlight or see how BusyKid stacks up against Greenlight. We also offer expert reviews on how FamZoo and Current measure up to market leaders.

If you are looking for a different approach, our guide to the best GoHenry alternatives will help you find the perfect fit for your family’s needs, ensuring your child builds the confidence to navigate the financial world.

Statistics on Financial Literacy in the UK

-

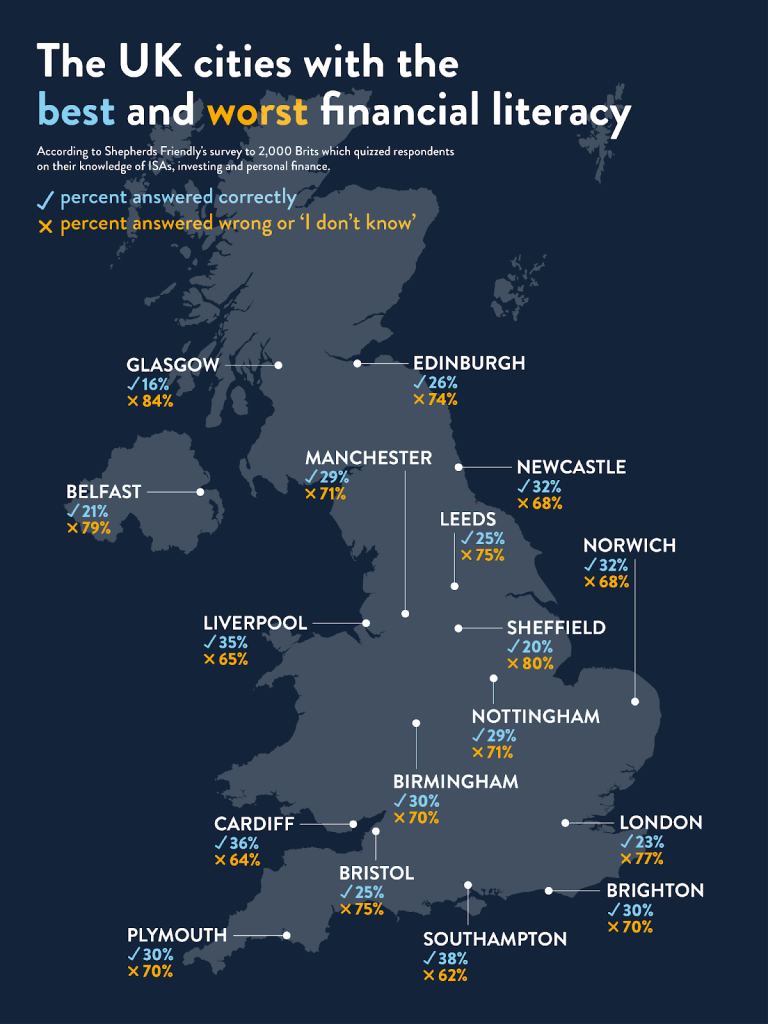

- Only 23% of Brits passed the latest financial literacy test [23], a sharp decline from 27% in 2023 and 49% in 2024. The survey, conducted by Shepherds Friendly Society in September 2025 with 2,001 UK adults, tested knowledge of ISAs, investing, insurance, income protection, and general personal finance, requiring at least half of 50 questions answered correctly. Fewer than 1 in 10 young people (aged 18–24) succeeded [23].

-

- 73% of Britons fall below the Financial Literacy Benchmark [24]. Research by Wealthify and the economic think tank CEBR, which surveyed 2,250 Britons on ten financial topics including inflation, taxes, pensions, and savings, found that nearly three-quarters fall below the minimum benchmark score, exposing the UK as a weak performer compared to similarly developed countries like France, Canada, and New Zealand.

-

- 39% of UK adults — roughly 20.3 million people — do not feel confident managing their money [25], according to the UK Financial Capability Strategy, cited in a major 2025 report by the London Foundation for Banking & Finance. The UK has significant gender, education, income, and ethnic gaps in financial literacy, with disparities of up to 45% when demographic factors compound [25].

-

- Older respondents perform the best on financial literacy tests [23]. Those aged 55 and above perform better than any other age group, while those aged 18–24 perform worst. Both generations still score poorly in absolute terms, with only 34% of those 55+ and just 8% of those aged 18–24 passing the most recent Shepherds Friendly test.

-

- There is a strong link between financial understanding and behavior [24]. Wealthify/CEBR research found that 7 out of 10 respondents with the highest level of financial literacy contribute to a pension, and those at the top of the benchmark save significantly more than those at the bottom.

-

- British men are more financially literate than women [23]. The 2025 Shepherds Friendly survey found that 29% of men passed the test compared to 17% of women. The gap was most pronounced in investing (40% of men vs. 26% of women) and income protection (22% of men vs. 14% of women).

-

- Only 19% of UK consumers can confidently explain common financial terms [26], according to Mintel’s 2026 UK Financial Education Consumer Report, even as 70% of consumers feel positive about their financial knowledge — a stark confidence-versus-competence gap.

Final Thoughts

The statistics above paint a clear and sobering picture: financial literacy remains critically low around the world in 2026, and in many cases is declining rather than improving. In the US, a decade of annual measurement shows almost no progress — adults answer the same share of financial questions correctly as they did in 2017. In the UK, the pass rate on a comprehensive money literacy test has fallen sharply over just two years. Meanwhile, the consequences of financial illiteracy are intensifying: household debt is at record levels, and financial anxiety is climbing across every demographic group.

The bright spots are in education policy. With 30 US states now mandating standalone personal finance courses for high school graduation — compared to just 6 states in 2019 — a generation of young people is beginning to receive structured financial education. The gender gap in financial literacy, visible as early as age 13, underscores how important it is to ensure these programs reach all students equally. Ultimately, the evidence is consistent: higher financial literacy leads to better savings behavior, lower debt, greater retirement readiness, and stronger overall financial well-being.